Three ways to meet changing customer expectations

Cost-of-living pressures remain a defining factor in the way customers shop, and price is still the number one concern. In fact, 64% of Australian customers list cost-of-living as their top worry, and many are actively adjusting their habits to make ends meet. This shift has real implications for product development. With cost-of-living pressures anticipated to persist, understanding how the market is shifting is crucial. If you’re developing or ranging products for today’s retail environment, here are three essential things to stay aligned with customer expectations and drive performance on-shelf.

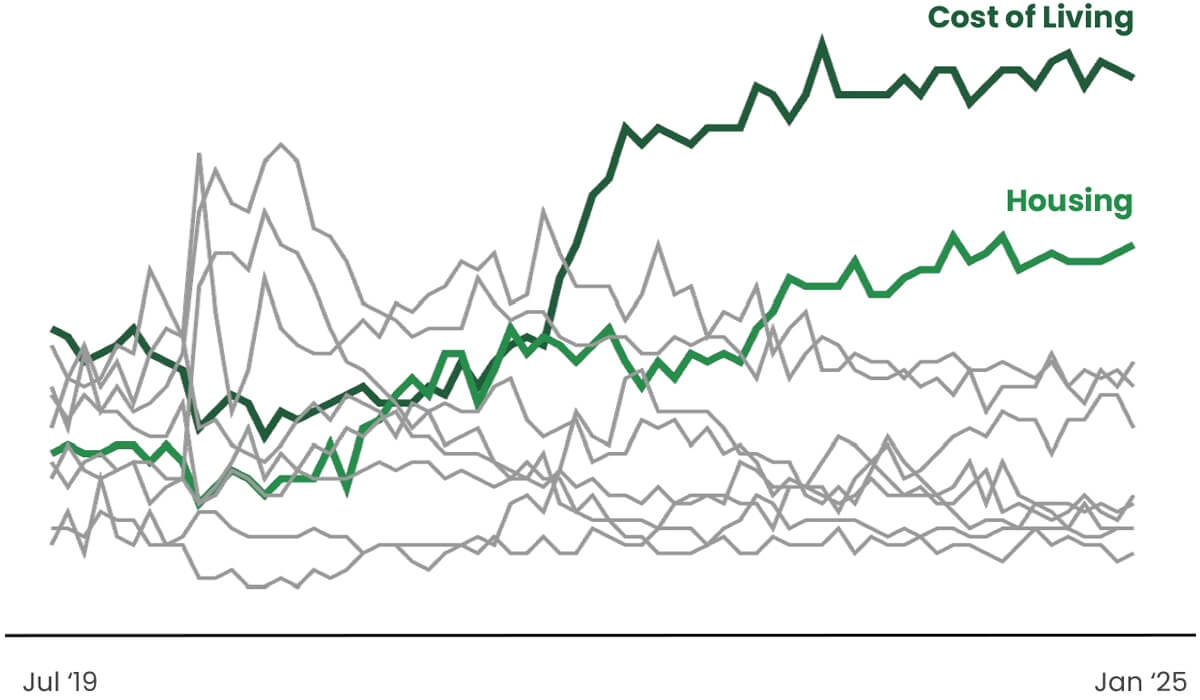

Cost of Living has been the top concern since May 2022

Top 5 issues specified by Australians (AU as of Jan 25)

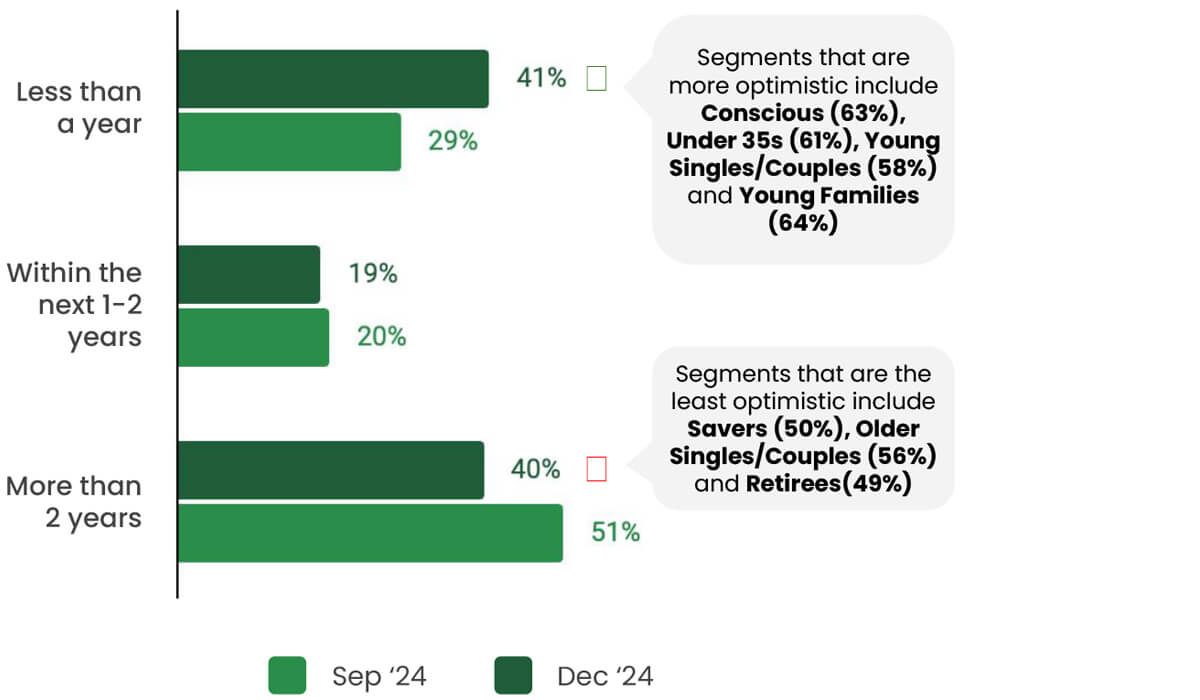

Cost of Living pressure are expected to continue

Expectation for COL pressures to ease (Discrete Month) (% Agreement Feb 2025)

Source: Qualtrics Consumer Pulse (Sample n = 1,006) | Fieldwork 3rd – 7th February 2025

1. Value is the priority

While many customers are exploring broader definitions of value, price remains the priority, particularly among key customer segments like Saver customers and Families, who are less willing to pay more for non-price benefits and are increasingly shopping around.

Customers are comparing: 36% say they’re buying more on promotion, while many are cutting back on treats, dining out and brand-name products.

Tip: Expect shoppers to shop around, compare, and make trade-offs. Strong price competitiveness seems to be the driving force of most everyday purchases, even when new product innovations are exciting customers. Even when adding features like sustainability or health benefits, affordability must come first—especially for core, high-volume ranges.

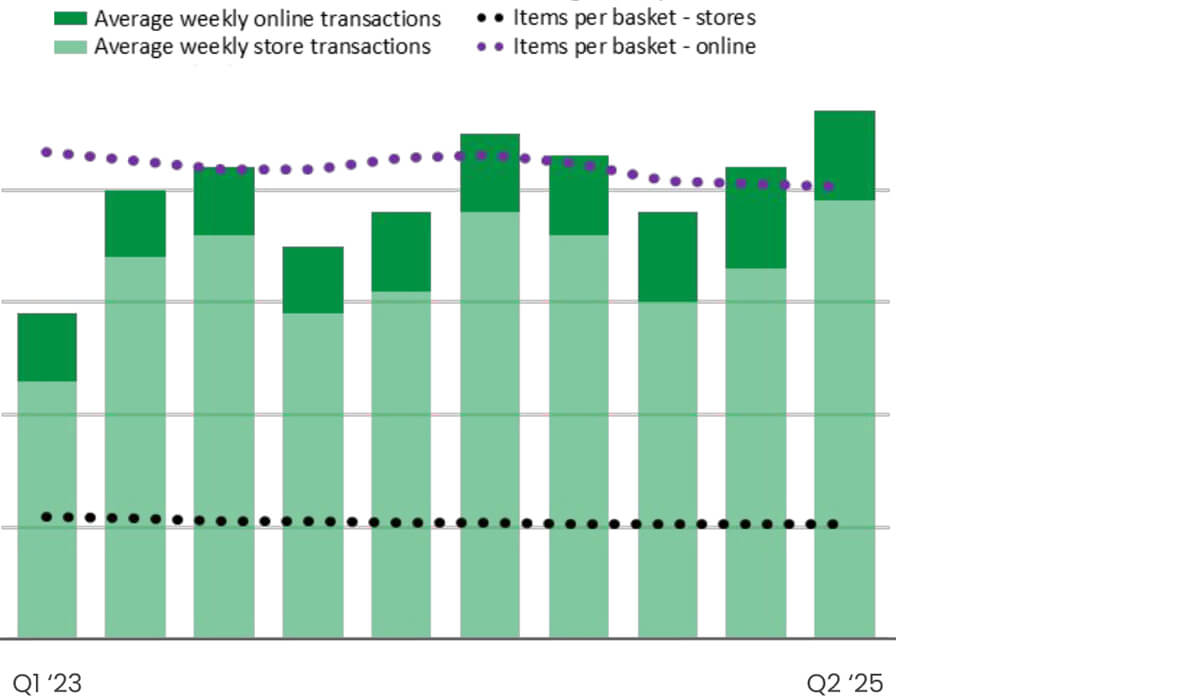

Customer Cross-Shopping Increasing

Cross Shopping (% of Customers claiming to shop more than one supermarket)

Shift to Conv & Smaller Baskets

Convenience (# of Transactions & Items per basket)

Source: * Qualtrics Consumer Pulse

Source: Q: When going grocery shopping (in-store and online), which of the following best describes your typical grocery shop?

Source: ** Excluding estimated impact of industrial action in Q2’25

2. Innovate through affordability

While some higher-income customer segments are showing a willingness to pay more for benefits like convenience, sustainability, or health, these represent a smaller portion of the customer base. The vast majority are still cost-focused and watching every dollar.

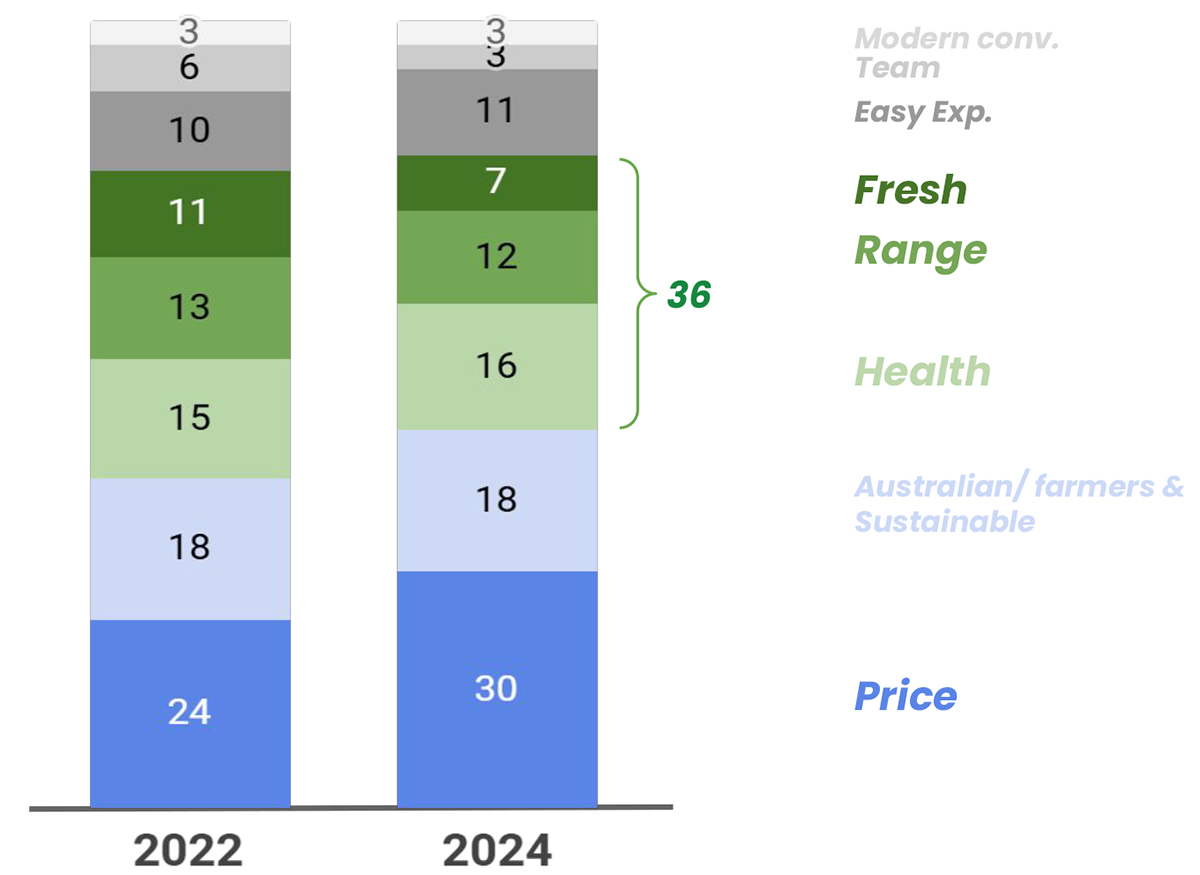

Drivers of Great Overall Value

Source: HOB WW Masterbrand Brand Health Tracker – Rational Perceptions Drivers Analysis

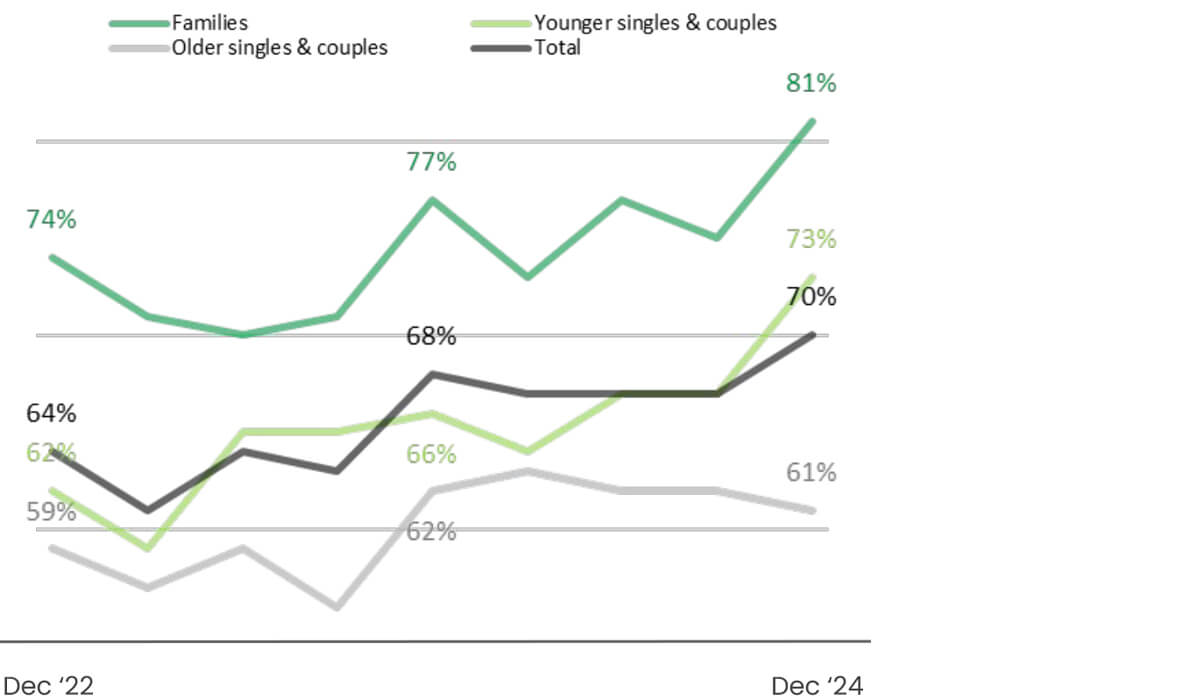

Cost of living and struggle to make ends meet are highest for families and younger customers. Saver customers and Families are trading down, and they’re doing it more often. Premium innovation can work, but only in the right parts of the store. For the rest, innovation needs to work harder to deliver compelling value as customers continue to hold concerns around financial pressures, and struggle to make ends meet.

Tip: Build from a foundation of affordability. Look for ways to innovate through smart packaging, efficient formats, or simplified ingredient sets that can reduce cost while still offering something new.

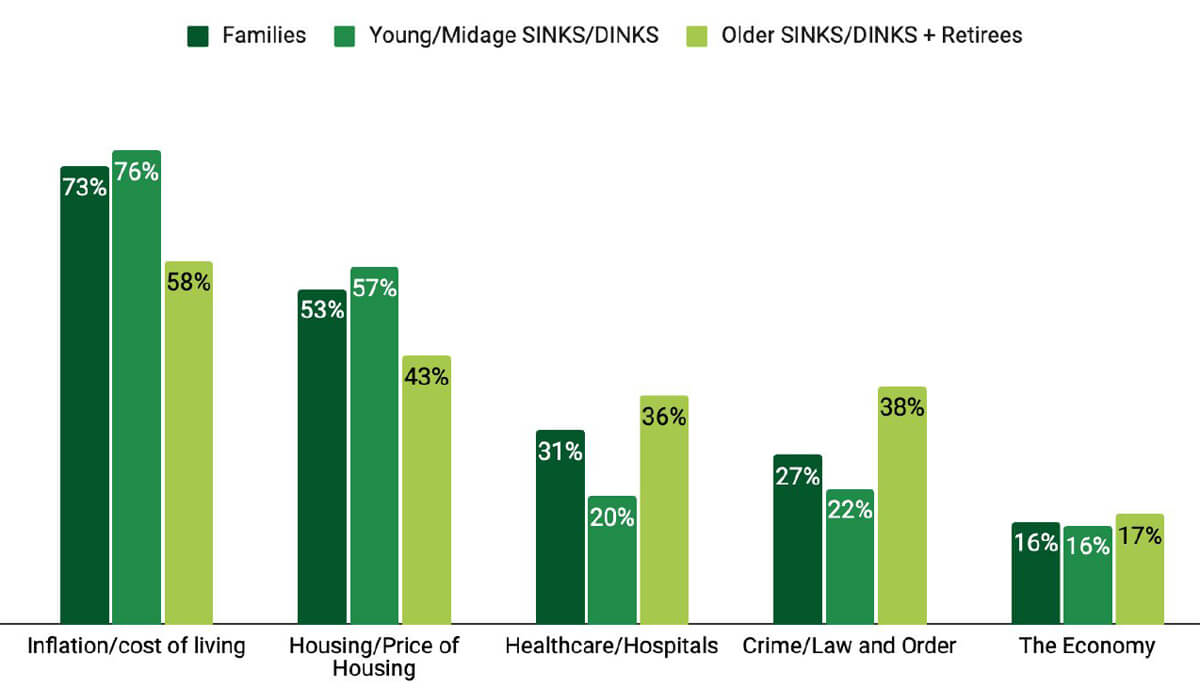

COL & Housing pressure highest for Families & Younger customers

Top 5 issues specified by customers in Australia – by Lifestyle (% respondents, Jan 2025)

STMEM highest within Families & Younger Customers

Struggle to make ends meet (STMEM) – by lifestyle (% respondents, Feb 2025)

Source: IPSOS Australia Issues Monitor (Question asks for top 3 issues) | January 2025

Source: Qualtrics Consumer Pulse (Sample n = 1,006) | February 2025

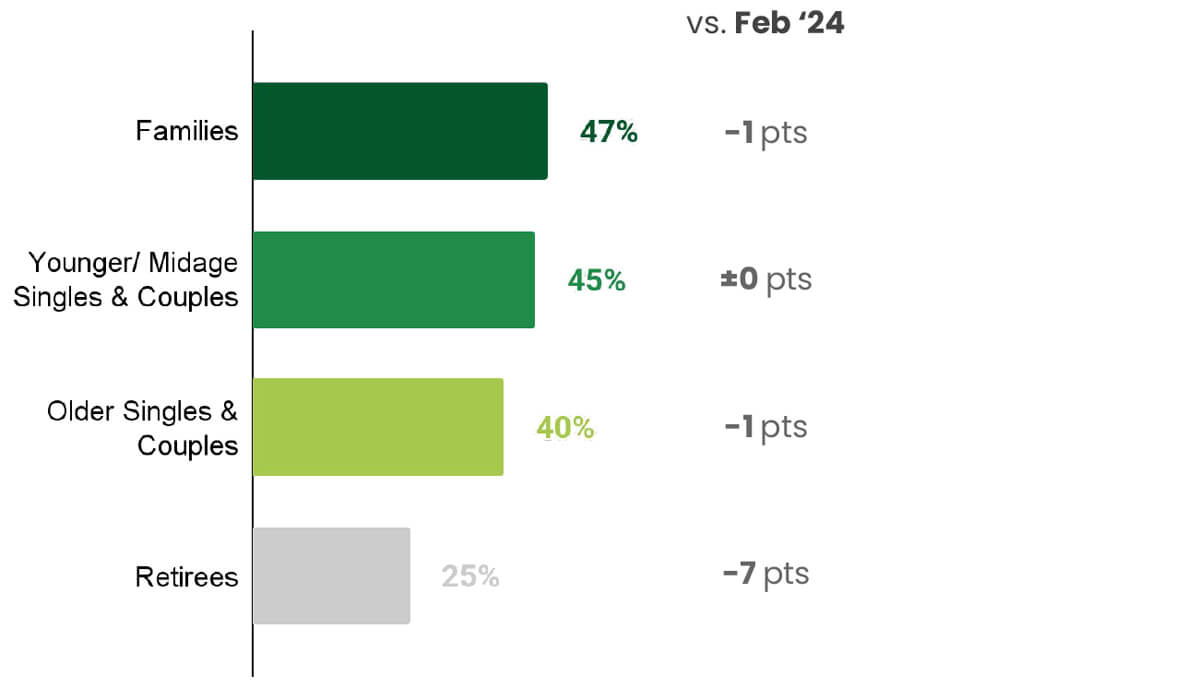

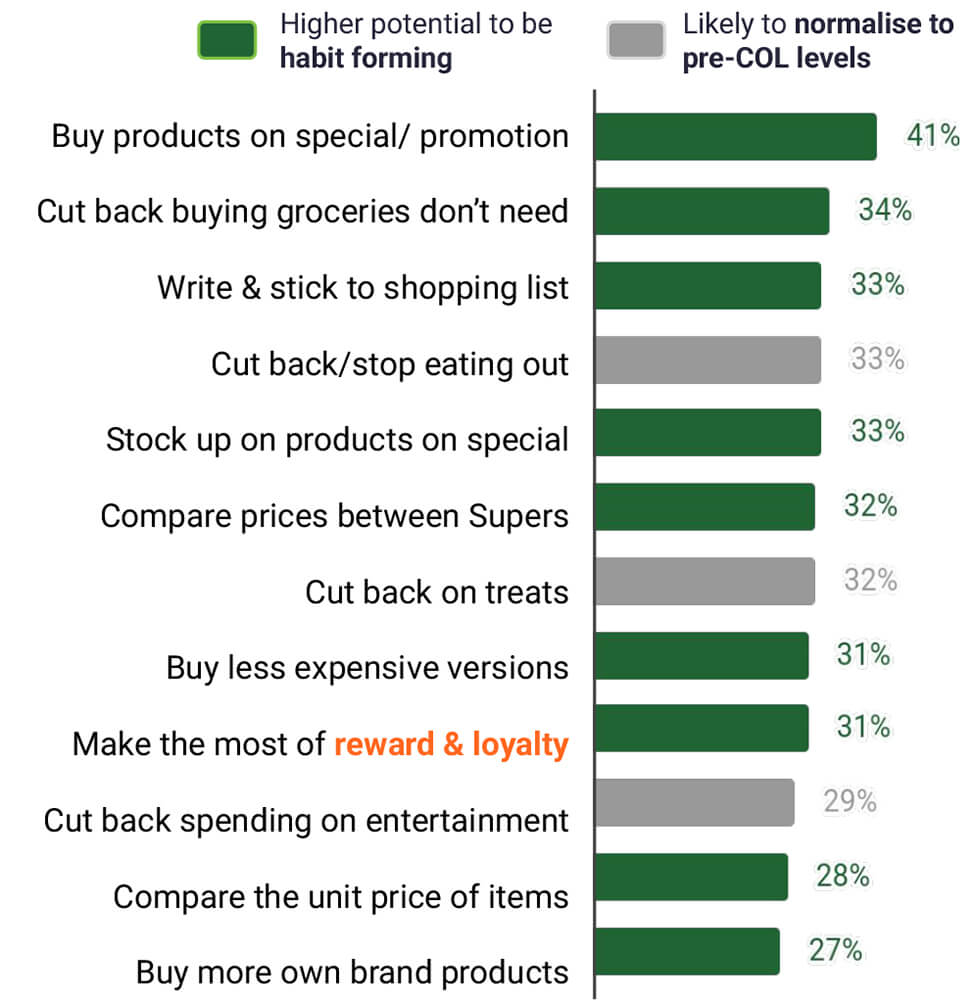

3. Plan for long-term, value-seeking customers

Many value-seeking behaviours adopted during the peak of the cost-of-living crisis have become entrenched. The average Woolworths customer still displays around 7 distinct value-seeking behaviours (compared to 5 pre-crisis).

Switching between retailers, seeking promotions, and trading into own brands are now the norm. Customers are not expecting prices to drop in the near term—and they’re behaving accordingly.

Tip: Position your products to meet this mindset. Think everyday low prices, multi-buy offers, and simple tiering strategies that make trading up a conscious choice rather than a stretch.

Top Value-Seeking Behavious Feb 25, 3MR

Source: Qualtrics Consumer Pulse n=1006 (Fieldwork: 3th-7th Feb): Q. In response to increasing prices of food, products & services, are you doing any of the following more than usual? Sig diff. At 95% CI ↑ Higher ↓ Lower. NOTE: CREST segments are not at complete alignment, CREST data 3 months rolled. Q. In response to increasing prices of food, products & services, are you doing any of the following more than usual? Sig diff. At 95% CI ↑ Higher ↓ Lower. NOTE: CREST segments are not at complete alignment, CREST data 3 months rolled.

While some shoppers are starting to reintroduce non-price considerations, value remains the key battleground. In order to grow with Woolworths customers today, products must meet evolving needs without compromising on affordability.